Stax Labs

Strategy Optimizer for Backtested Investing Rules

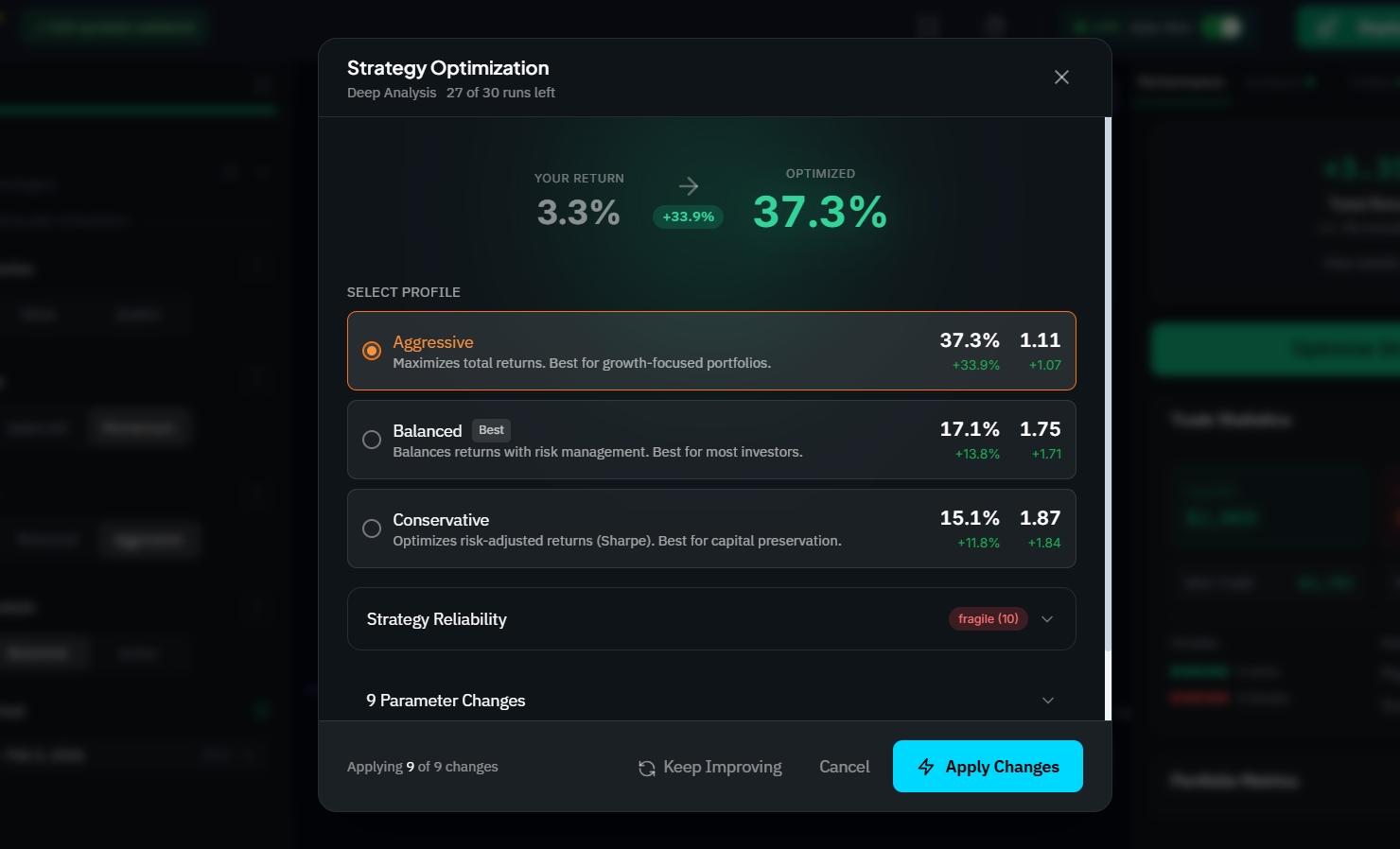

Optimization is useful only when it makes a strategy more understandable. Stax helps users compare parameter choices, see tradeoffs, and avoid treating the highest backtest as a magic answer.

What users get

- Focus

- Parameters

- Compare

- Return + risk

- Guardrail

- Overfit aware

The job it solves

Test strategy parameters, compare outcomes, and understand which rules improved risk-adjusted performance without losing sight of overfitting risk.

Built for the actual investing workflow

Stax is strongest when a visitor can move from learning to building to testing without switching tools or losing the original idea.

Compare stop loss, rebalance, ranking, and sizing choices.

Find parameter regions that are robust instead of one lucky point.

Understand why a setting improved or hurt the result.

Apply better settings back to the strategy builder.

How it works

A practical path from an idea to evidence, then from evidence to practice.

- 1

Start with a strategy that already has a clear thesis.

- 2

Choose the parameters worth testing and the ranges that make sense.

- 3

Compare outcomes across return, drawdown, Sharpe ratio, and stability.

- 4

Apply the best-supported changes and retest the full strategy.

Optimization is connected to real strategy rules, not isolated spreadsheet knobs.

Risk-adjusted metrics sit beside returns so users do not chase fragile settings.

The workflow encourages explanation before deployment.

Learn the concepts behind the tool

Start with a template

Questions people ask

What is strategy optimization?

Strategy optimization compares different parameter choices to see how they affected historical performance, risk, and consistency.

Can optimization cause overfitting?

Yes. Overfitting happens when a strategy is tuned too closely to the past. A good optimizer should make tradeoffs visible instead of hiding them.

What should I optimize first?

Start with parameters that match the strategy thesis, such as rebalance frequency, position count, ranking weights, or risk exits.

Ready to use strategy optimizer for backtested investing rules?

Start with a clear idea, test the rules, and keep the risk visible before the decision gets emotional.